Benefits

Fulfillment of the requirements of the 4th AML Directive

The system allows for fulfillment of requirements of the newest AML Directive on counteracting money laundering and terrorism financing in the area of AML risk assessment calculation and management.

Full AML risk assessment process

PS AML provides support for the full AML risk assessment process - from assessing a new customer, through meeting the requirements for increased customer identification and verification, handling sanction lists and PEP (politically exposed persons), cyclical customer assessment and transaction monitoring.

Ready-made risk assessment models

The system has implemented risk assessment models adequate to the stage of cooperation with customers, including those based on behavioral assessment of customers.

Integration of EDD surveys into the KYC process

Automatic adjustment of the content of KYC surveys according to online AML risk assessment. Access to surveys for persons conducting the customer's onboarding process from the level of the supported CRM system. Survey results are available for AML officers directly in the case handling module.

High-performance solution architecture

The technologies used allow the system to be deployed in a high-performance environment. This allows for safe integration with operating systems in organizations. As a result, the risk assessment of a new customer and transaction monitoring are completed in milliseconds.

Meeting the needs of the compliance department

An integral part of the environment is the alert management module dedicated to the AML team working in compliance departments. It allows for handling cases indicating a higher risk of money laundering, so that alerts are adequate to the type of the case (new customer, EDD, existing customer, transaction monitoring, EDD).

Security

PS AML has been developed for years. It has successfully passed inspections of supervisory institutions on several occasions. It allows for efficient auditing and demonstrating that the institution meets the requirements of the Act on Counteracting Money Laundering and Terrorism Financing, thereby protecting the company in the event of an inspection and minimizing the risk of penalties.

Flexibility

The software can be customized to suit your organization's needs. it is possible to add and remove rules, patterns, risk models, use one's own and external blacklists or configure alerts.

Versatility

The PS AML solution supports anti-money laundering efforts not only in the largest financial institutions in Poland, but also in Germany, the Czech Republic, Slovakia, Hungary and Romania.

For whom?

System Security Office

Money laundering risk assessment is carried out when establishing cooperation with each new customer, with the exception of designated institutions, countries and administration.

When undertaking cooperation with a new customer, the obliged institutions need to carry out basic customer identification and verification. In this procedure, it is possible to assess the risk of a customer's relationship with money laundering and thus decide whether to use the standard procedure or to undertake enhanced identification and verification through the KYC process or, where appropriate, to refuse to cooperate. PS AML provides full support for the identification, verification and risk assessment of new customers online, including context-dependent EDD (Enhanced Due Diligence) surveys.

Monitoring and assessing the risk of money laundering makes it possible to manage potential threats by subjecting customers to controls and supervision commensurate with the risk.

PS AML makes it easy for organizations to detect changes that may affect the assessment of the risk assigned to a customer. Such changes may include, for example, changes in personal data, new linkages between entities, blacklisting or emergence of risky behaviors. If they occur, the risk assessment for the customer is changed accordingly in PS AML.

Continuous ongoing efforts to address potential risks of money laundering and terrorism financing related to customers and contractors, products and services as well as geographical areas of activity.

The scope of transaction monitoring depends on the level of customer risk. Increased monitoring is carried out in the case of high-risk customers. For low-risk customers, the rigor is reduced. For selected groups of transactions (e.g. foreign transactions) and for selected groups of customers (e.g. persons holding politically exposed positions, the so-called PEP, present on the black lists), continuous monitoring is applied. Transactions in all communication channels are analyzed.

Offered functions

Risk assessment of a new customer

PS AML provides comprehensive support for automatic risk assessment for new customers. It is based on appropriately calibrated, ready-to-use risk assessment models taking account of, among others, the following product, geographic and industry risk factors. Both basic and enhanced customer identification and verification are ensured.

Real time assessment calculation

Using appropriate technologies, the risk assessment is calculated in real time, with a proper secure and high-performance architecture provided.

Handling of sanction lists and PEPs

The system supports a wide range of sanction and PEP lists available on the market. Appropriate access interfaces to different data formats are provided. Each of the implemented risk assessment models takes account of the rules related to the presence of persons and entities on the sanction lists.

KYC/EDD surveys

The requirements of enhanced customer identification and verification are ensured by automatically triggering risk level- and customer type-dependent EDD surveys. Integration with external systems has been minimized by the use of the dynamic authorization technology. This reduces the cost of adjusting the front end systems.

Managing user's own blacklists

PS AML provides the functionality to manage and maintain the user's own blacklists, allowing flexible supplementation of the imperfections visible on the lists available on the market.

Periodic customer assessment

PS AML provides automatic customer risk assessment based on extensive rules and benchmarks. Automatic analysis includes detection of events and changes that may affect customer risk assessment, including STIR risk assessment. The effect of the cyclical assessment is proper risk-based transaction monitoring.

Calculation of behavioral factors

As part of the cyclical evaluation of customers, patterns catching suspicious behaviors of customers are very strongly developed. The system implements a number of templates that can be freely adapted to the particular industry and activity.

Transaction monitoring

Based on the periodical customer assessment, the system performs adequate verification of customer transactions, and the scope, detail and frequency of monitoring depend on the risk assessment: customers, products and realization channels (risk-based approach).

Calculation of typical behavior profiles

The system implements rules calculating the level of deviation from typical customer behavior profiles based on transactional data. For high-risk customers, a respective small deviation from typical behavior can result in additional alerts being sent to the AML team.

Periodical customer review

The system supports periodical customer reviews. Their level and manner of implementation depends on the customer risk level. Information collected by means of dedicated surveys is archived in PS AML.

Verification of increments on the sanction lists and PEP lists

Persons and entities on sanction and PEP lists are monitored daily, fully automatically in the system. It is possible to enable the fuzzy matching algorithm, which allows for a controlled margin of deviation from the record being compared.

Verification of inactive PEPs

The relevant algorithms automatically check whether the status of the identified PEP should not be changed to inactive. The system provides all the information and details of a person suspected of becoming an inactive PEP, which facilitates decision making.

Monitoring of foreign transactions

The system is adapted to on-line monitoring of foreign transactions through SWIFT/SEPA channels. Suspicious transactions are put aside for in-depth analysis.

Alert management, AML case management

PS AML has an extensive case management system, tailored to AML needs, integrated with analytical engines and external systems. It allows for providing information to persons verifying cases, returning risk assessment results, managing the process of further case handling and archiving.

Management of notifications to GIIF

The system provides the functionality of recording reports of suspicious and related transactions to GIIF . This facilitates the management and control of the sent cases and the list of reported entities is used as a factor in risk assessment.

Management of inquiries from GIIF and the Public Prosecutor's Office

PS AML enables the collection of queries from GIIF and the Public Prosecutor's Office. This function is useful for checking the process of preparing responses. Queries can be entered in manual or batch mode.

Internal reporting

The reporting area implemented in the system ensures quick and convenient preparation of management reports. There is a possibility of using a number of predefined reports related to case handling in different AML areas and a possibility of generating the user's own "ad-hoc" reports, depending on preferences and needs.

Collection of information on refusals to cooperate

The system supports the management of refusals to start cooperation by the ability to collect information on refusals. A dedicated interface allows the user to browse and search for information conveniently, and the information collected is included in the periodical risk assessment.

Flexible adaptation to individual requirements

The applied technologies allow for quick adjustment of the system to the individual needs of customers. From the ability to easily change ETL structures, to the ease of expansion and calibration of AML/CFT risk models, to the customization of the processes handled in the case handling module.

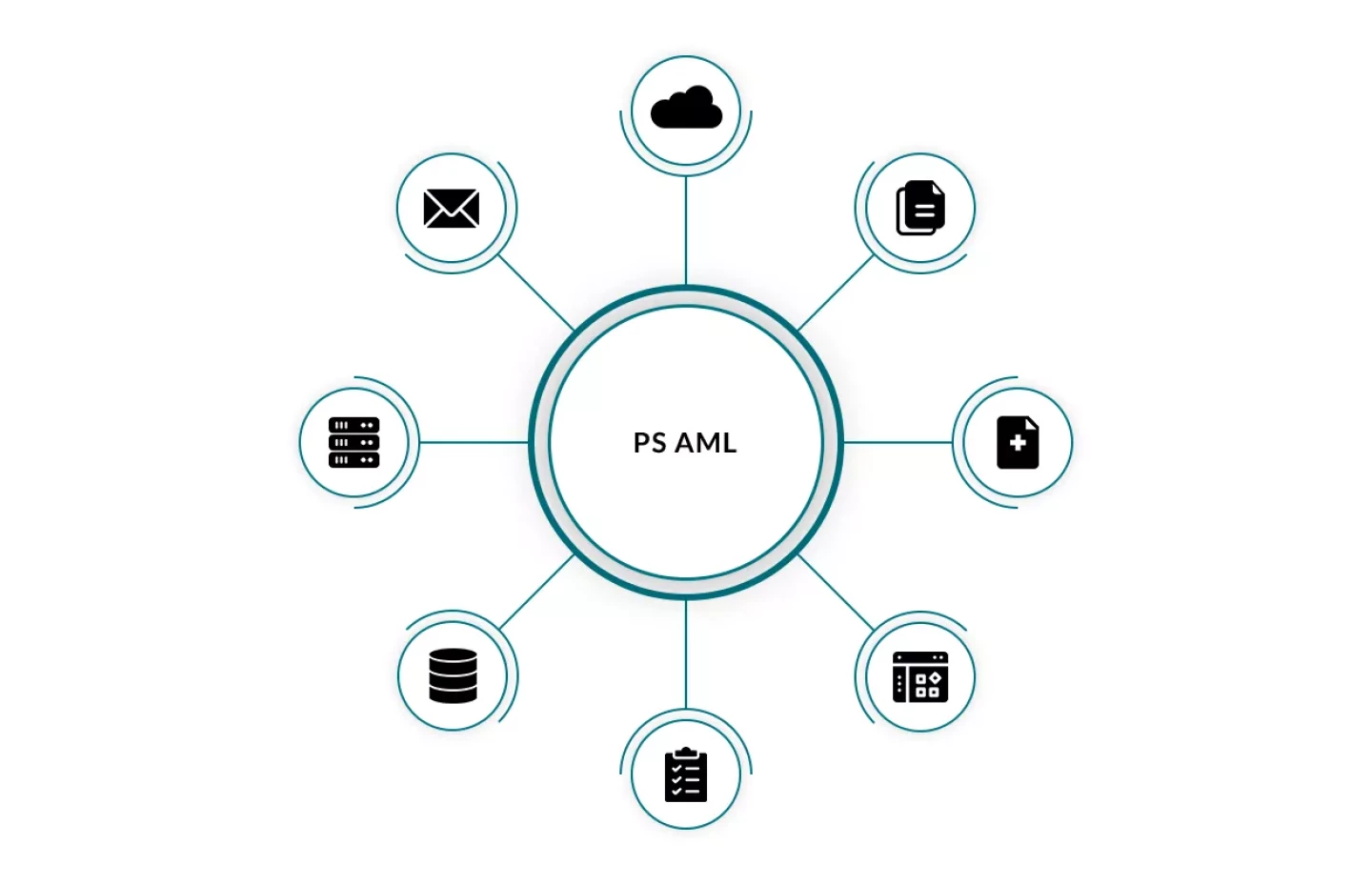

Integration with systems

PS AML has implemented a wide range of integration options with external systems, from integration through WebServices/REST, to efficient file gateways or data-based integration.

Industry-based customization

The system is adapted for use within a wide range of industries, with particular emphasis on the banking sector, including specialist mortgage, leasing, factoring, brokerage and insurance banking.

Predictive studies

The system implements the options of performing advanced studies using segmentation and prediction or sequential algorithms. The first three can be very effective in identifying new areas of abuse and increasing the effectiveness of risk models.

Reporting suprathreshold transactions to GIIF

The system ensures compliance with new requirements related to the registration of suprathreshold transactions at GIIF and keeping the register in the obliged institution.